You are here

Direct Program, Direct Administrative, and Indirect Costs

Frequently Asked Questions (FAQs)

- Compensation (i.e., salary and benefits) for employees who work on the program or deliver services/supports to students served by the program;

-

Cost of trainings or professional development for employees working on the program;

-

Cost of supplies and materials necessary specifically for the purpose of the program;

-

Equipment purchased and used for the program (inventoried and tracked);

-

Travel expenses incurred specifically to carry out the program, etc.

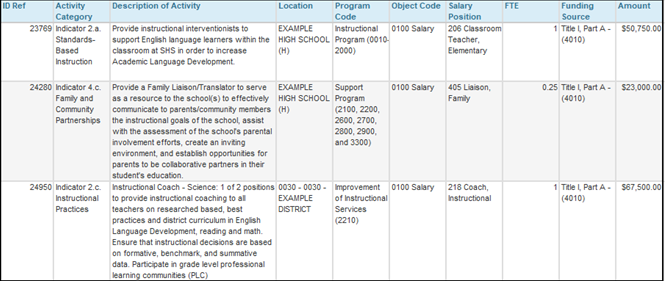

Below are examples of direct program costs, as budgeted in the Consolidated Application platform:

Figure 1: Example of direct program costs budgeted in Consolidated Application

Direct Administrative Costs

What are direct administrative costs?

Direct administrative costs are costs associated with the administration of a program, but do not serve students directly. Direct administrative activities include, but are not limited to:

- Overall program management, including salaries and related costs;

- Activities concerned with paying, transporting, exchanging, and maintaining goods and services;

- Activities concerned with establishing and administering policy, preparing reports, etc.;

- Activities related to the program requirements of grantees.

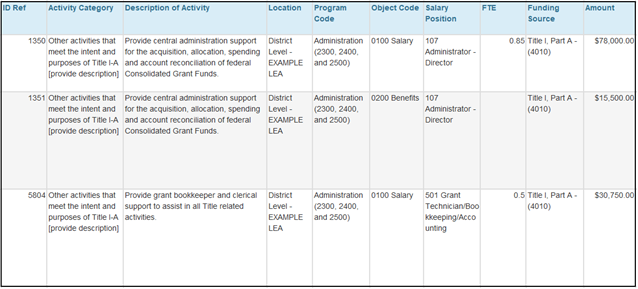

Note: There is an important distinction between direct administrative costs (e.g., program codes 2300, 2400, 2500) and direct program costs associated with support functions. For example, program coordination or program evaluation activities are considered support functions (program codes 2100, 2200, 2600, 2700, 2800, 2900, 3300) – rather than direct administrative costs. Specific examples of direct administrative program costs, as budgeted in the Consolidated Application platform, are provided below:

Figure 2: Example of direct administrative costs budgeted in Consolidated Application

How do I budget direct administrative costs?

Direct administrative costs for each Title program may be budgeted in the Consolidated Application as individual line items under the appropriate Title program funds page using the program code “Administration.”

Indirect Costs

What are indirect costs?

Indirect costs are costs necessary to provide a service but may not be readily identified with or easily allocable to a particular cost objective for a Title program. Indirect costs include, but are not limited to: goods and services required for program administration, including the rental or purchase of equipment (unless purchased for direct program services or activities, which should be identified as direct program costs – see above), utilities, office supplies, postage, and rental or maintenance of office space, etc.

Before the indirect cost rate for each LEA can be set, the Colorado Department of Education’s (CDE) methodology has to be approved by the US Department of Education’s Indirect Cost Rate Group. Once the methodology is approved, CDE determines the indirect cost rates for each LEA that submits a finance data file to CDE in December. (See CDE school finance web page here: https://www.cde.state.co.us/cdefinance/icrc).

Indirect costs are automatically calculated by multiplying the rate by items charged directly to the program, excluding items categorized as capitalized equipment (Object Code 0730). The calculated amount is viewable on the Budget Summary page of the ESEA and ESSER applications. The amount calculated is automatically budgeted and can be reduced or removed if necessary. A local education agency’s (LEA) indirect cost rate does not vary across Title programs.

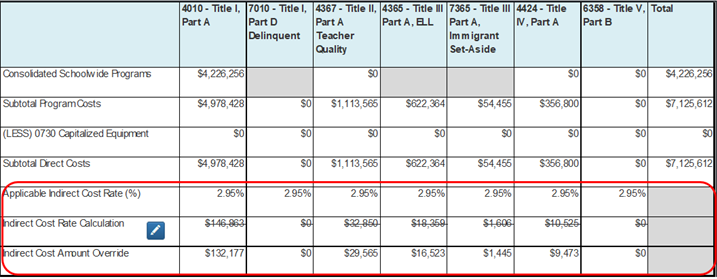

CDE pre-populates the online platform with an indirect cost rate for each LEA. The rate may be viewed and edited on the LEA Profile page in the Consolidated Application however, the rate cannot be changed in the ESSER application. Indirect cost rates for each fiscal year are also available on the CDE School Finance website. Below is an example of an LEA’s indirect cost rate, as it appears in the Consolidated Application:

If an LEA elects to override the indirect cost rate set by CDE, the adjusted rate must be less than the CDE pre-populated rate. In addition to the LEA Profile page, indirect cost amount can also be modified in the Budget Summary page by using the blue edit button next to the “Indirect Cost Rate Override” line item. The Consolidated Application platform will strikethrough the original indirect cost calculation to indicate that the amount has been overridden whereas the ESSER application system will display the calculated amount and the revised amount. LEAs that do not intend to take any indirect costs may find it more convenient to enter “0” for the indirect cost rate in the LEA profile section of the Consolidated Application, eliminating the need to override the indirect cost amount in the Budget Summary. An example of a modified indirect cost rate, as it appears in the Budget Summary page of the Consolidated Application, below:

Figure 4: Example of modified indirect cost rate in Consolidated Application Budget Summary page

Below is an example of the ESSER Fund Budget page that shows the calculated indirect cost rates and override option.

Figure 4a: Example of indirect cost rate in ESSER Application system

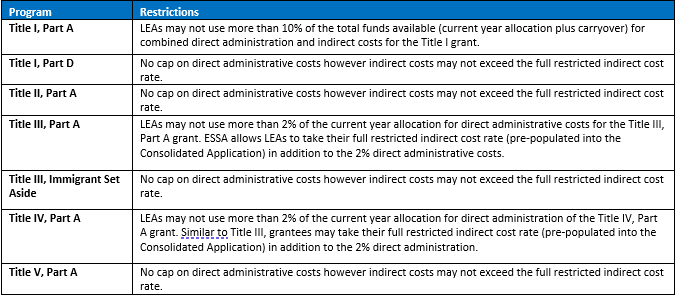

Direct administrative and indirect costs are restricted at different levels for different federal programs. Budgeted direct administration cost totals can be viewed on the budget summary page of the Consolidated Application, under the Administration section, as can indirect costs at the bottom of the page. See Figure 5 below:

Figure 5: Indirect cost and administrative cost restrictions, by Title program

To what extent can I modify direct administrative or indirect costs from year to year?

LEAs must be consistent in designating costs as direct administrative or indirect costs under Federal awards. Once designated as direct or indirect, costs should be treated consistently for all projects and activities, regardless of funding source.

For more information related to direct program, direct administrative or indirect costs, contact your ESEA Regional contact or the Office of Grants Fiscal.

Financial information on schools and districts throughout Colorado. Learn more about financial transparency.

Colorado Dept. of Education

201 East Colfax Ave.

Denver, CO 80203

Phone: 303-866-6600

Contact CDE

CDE Hours

Mon to Fri, 8 a.m. to 5 p.m.

See also Licensing Hours

UPDATED

March 30, 2022

Copyright © 1999-2025 Colorado Department of Education.

All rights reserved.

Title IX.

Accessibility.

Disclaimer.

Privacy.

Connect With Us